Section 18 Plotting with R (I):

ggplot2

Prerequisites

Load the libraries with R:

## Warning: 程序包'gapminder'是用R版本4.5.2 来建造的This section is modified from the excellent Data

visualisation and How to make

any plot in ggplot2?, both are freely available

online.

ggplot2 is the most elegant and aesthetically pleasing

graphics framework available in R. It implements the grammar of

graphics, a coherent system for describing and building graphs.

It can significantly improve your plots’ quality and make you much more

efficient in creating them. With that being said, the learning curve is

steep because the way you make plots with ggplot2 is very

different from base graphics making in R and in other languages. The

distinctive feature of the ggplot2 framework is the way you

make plots through adding layers. Here we will learn

the steps of making a plot with ggplot2. More about

ggplot2, check How to make

any plot in ggplot2?.

Steps of plotting with ggplot2

1. Passing the data set

First of all, you need to tell R what data set to use in plotting.

This is done by passing a data.frame object to the

ggplot() function. Here the data frame object should

contain all features needed to make the plot you want.

Unlike base graphics in R and other languages, ggplot()

does not take vectors as arguments.

In previous sections, you learn how to use the pipe operator

(%>%) to pass a data set (tibble object)

produced through data wrangling to

the ggplot() function. This is exactly what you need to do

in this step.

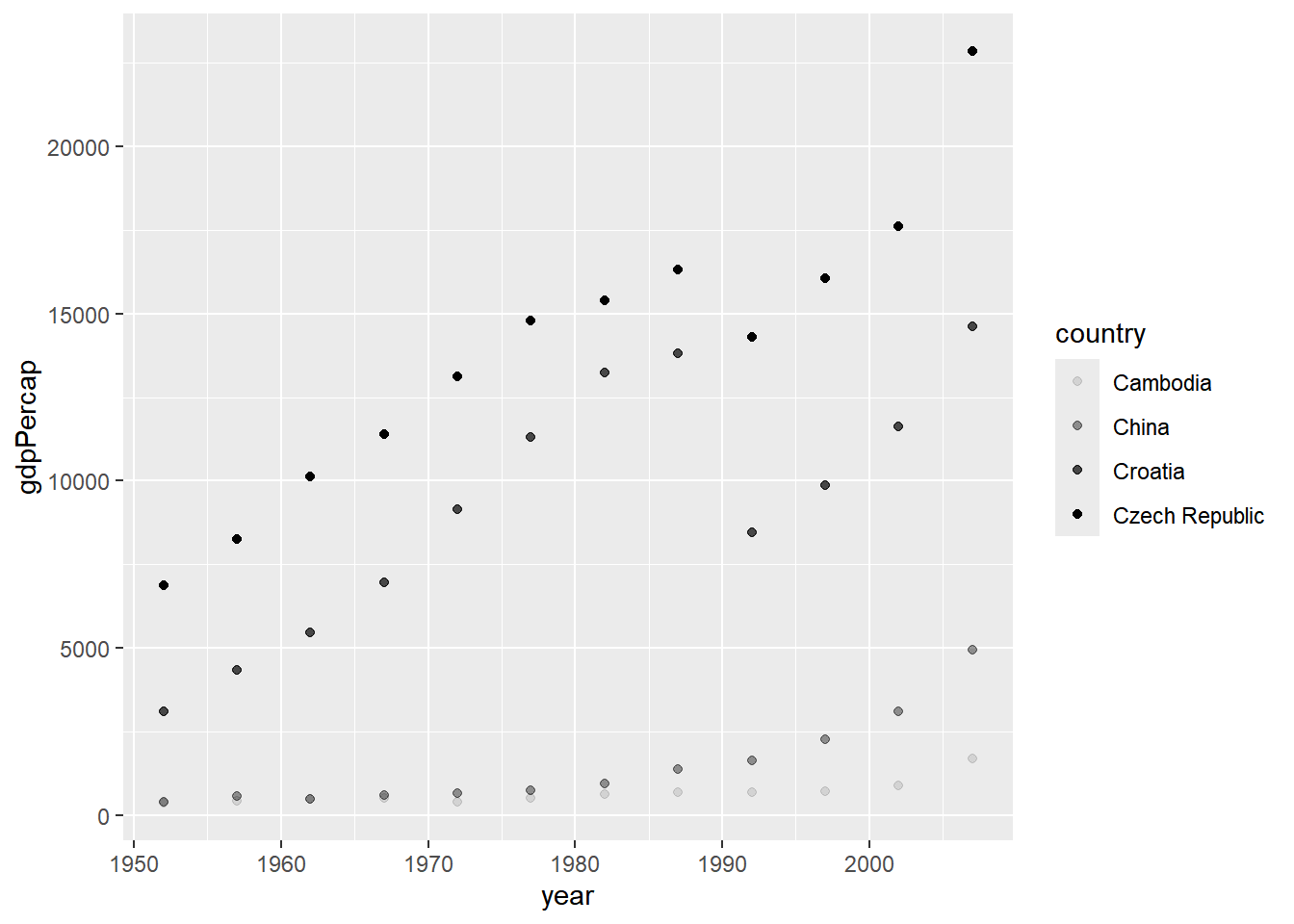

Let’s use the gapminder data set. Now suppose we want to

look at how GDP per capita (gdpPercap) changes from 1957 to

2007 for countries with names starting with the letter “C” in Asia or

Europe. (I make up this subjective example, but hopefully, you can feel

the power of the dplyr package!) We can then pass the

subset of gapminder data to ggplot to make a

scatter plot between gdpPercap and year.

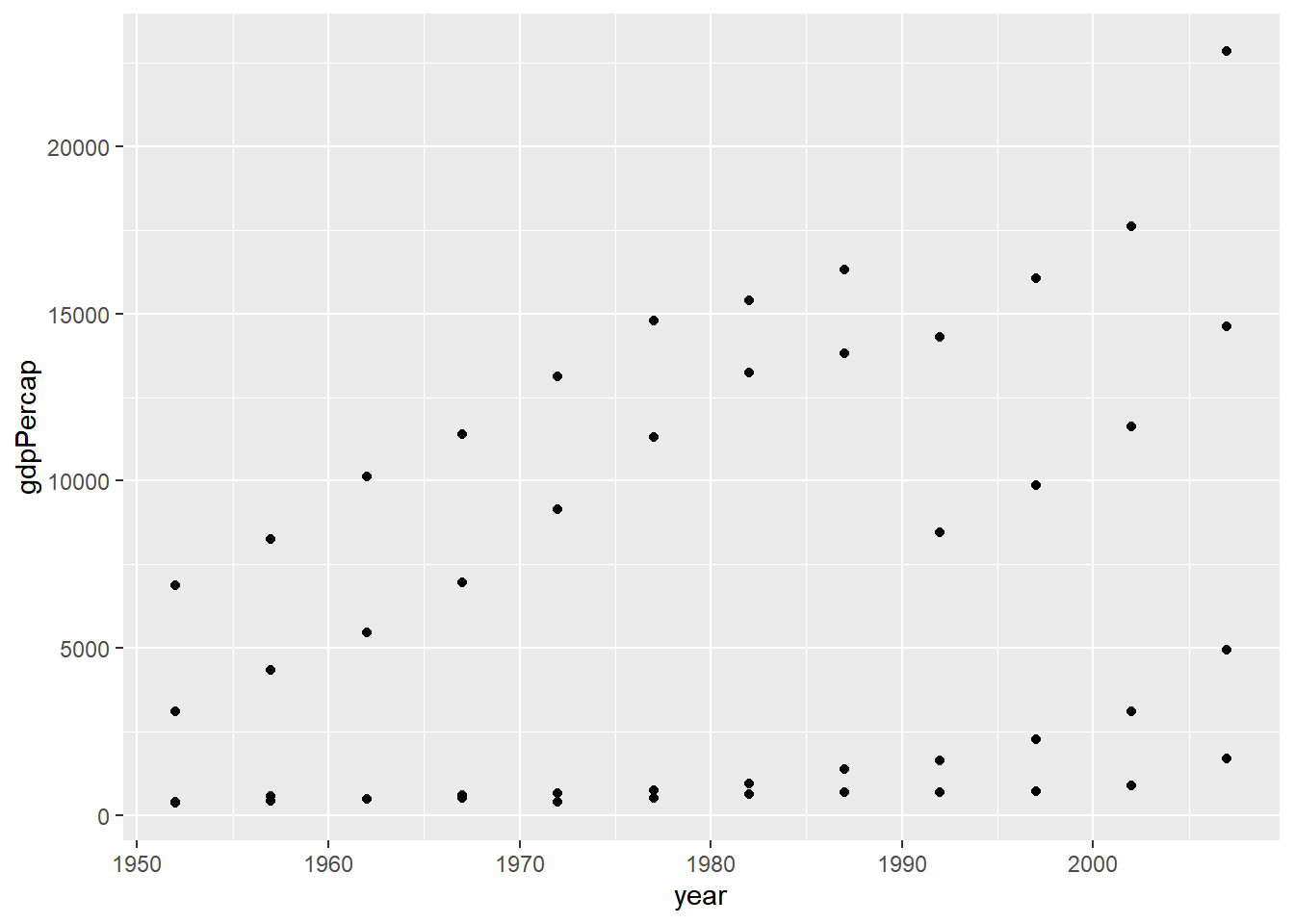

# Make a simple scatter plot

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap) ) +

geom_point()

2. Mapping the aesthetics

The plot above, however, can not distinguish countries as all points

are plotted in the same manner. In fact, we would like to add

country as the third variable to the two dimensional

scatter plot. By doing so, we are mapping the scatter plot to an

aesthetic. An aesthetic is a visual property of the objects in

your plot. Aesthetics include things like the size,

shape, color, or even transparency

(alpha) of the points. You can display a point (like the

one below) in different ways by changing the values of its aesthetic

properties.

# Add an aesthetic - color

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country) ) +

geom_point()

To map an aesthetic to a variable, associate the name of the

aesthetic to the name of the variable inside aes().

ggplot2 will automatically assign a unique level of the

aesthetic (here a unique color) to each unique value of the variable, a

process known as scaling. ggplot2 will also add a

legend that explains which levels correspond to which

values.

In the above example, we mapped country to the

color aesthetic, but we could have mapped

country to the size aesthetic in the same way.

In this case, the exact size of each point would reveal its class

affiliation.

# Add an aesthetic - size

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, size=country) ) +

geom_point()## Warning: Using size for a discrete variable is not advised.

We get a warning here, because mapping an unordered variable

(country) to an ordered aesthetic (size) is

not a good idea. We can ignore the warning for now.

Similarly, we could map country to the

shape or alpha aesthetic:

# Add an aesthetic - shape

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, shape=country) ) +

geom_point()

# Add an aesthetic - transparency

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, alpha=country) ) +

geom_point()## Warning: Using alpha for a discrete variable is not advised.

You can even combine more than one aesthetic:

# Add two aesthetics - color + shape

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country, shape=country) ) +

geom_point()

# Add two aesthetics - shape + size

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country, shape=continent, size=country) ) +

geom_point()## Warning: Using size for a discrete variable is not advised.

Once you map an aesthetic, ggplot2 takes care of the

rest. It selects a reasonable scale to use with the aesthetic, and it

constructs a legend that explains the mapping between levels and

values.

3. Adding more geometric objects

In the previous steps, we make a scatter plot between

gdpPercap and year. The plot uses a visual

object to represent the data. In ggplot2 syntax, we say the

plot uses a geometrical object or geom.

People often describe plots by the type of geom that the plot uses.

For example, bar charts use bar geoms, line charts use line geoms,

boxplots use boxplot geoms, and so on. ggplot2 provides

over 40 geoms, and extension packages provide even more (see here for a

sampling). The best way to get a comprehensive overview is ggplot2

cheatsheet. To learn more about any single geom, use ?,

for example ?geom_smooth.

In ggplot2, you can use “+” to add another geom to the

plot. In the plot below, we add a smoothed line to the scatter plots

from the individual country.

# Use two geoms - point + smooth line

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country) ) +

geom_point() +

geom_smooth()## `geom_smooth()` using method = 'loess' and formula = 'y ~ x'

4. Changing the labels

Now that you have drawn the main parts of the plot. You might want to

add the plot’s main title and perhaps change the X and Y axis titles.

This can be accomplished using the labs layer, meant for

specifying the labels. However, manipulating the size, the color of the

labels is the job of the ‘Theme’.

# Change labels

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country) ) +

geom_point() +

geom_smooth() +

labs(title="GDP per captia from 1957 to 2007", x="Year", y="GDP per captia")## `geom_smooth()` using method = 'loess' and formula = 'y ~ x'

5. Adjusting the theme

Very often, we want to customize our plot to make it looks better.

For example we may need to increase the size of the labels and/or change

the legend title. Adjusting the size of labels can be done using the

theme() function by setting theplot.title,

axis.text.x, and axis.text.y option. They need

to be specified inside the element_text(). If you want to

remove any of them, set it to element_blank(), and it will

vanish entirely.

Adjusting the legend title is a bit tricky. If your legend is that of

a color attribute and it varies based on a factor, you need

to set the name using the

scale_color_discrete() function, where the color part

belongs to the color attribute and the discrete because the

legend is based on a factor variable.

# Change the theme

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country) ) +

geom_point() +

geom_smooth() +

labs(title="GDP per captia from 1957 to 2007", x="Year", y="GDP per captia") +

theme_bw() +

theme(plot.title=element_text(size=20, face="bold"),

axis.text.x=element_text(size=10),

axis.text.y=element_text(size=10),

axis.title.x=element_text(size=20),

axis.title.y=element_text(size=20)) +

scale_color_discrete(name="Country Name")## `geom_smooth()` using method = 'loess' and formula = 'y ~ x'

6. Using the facets

For categorical variables, it is particularly useful to split your

plot into facets, subplots that each display one subset of the

data. To facet your plot by a single variable, use

facet_wrap(). The first argument of

facet_wrap() should be a formula, which you create with

~ followed by a variable name. The variable that you pass

to facet_wrap() should be discrete.

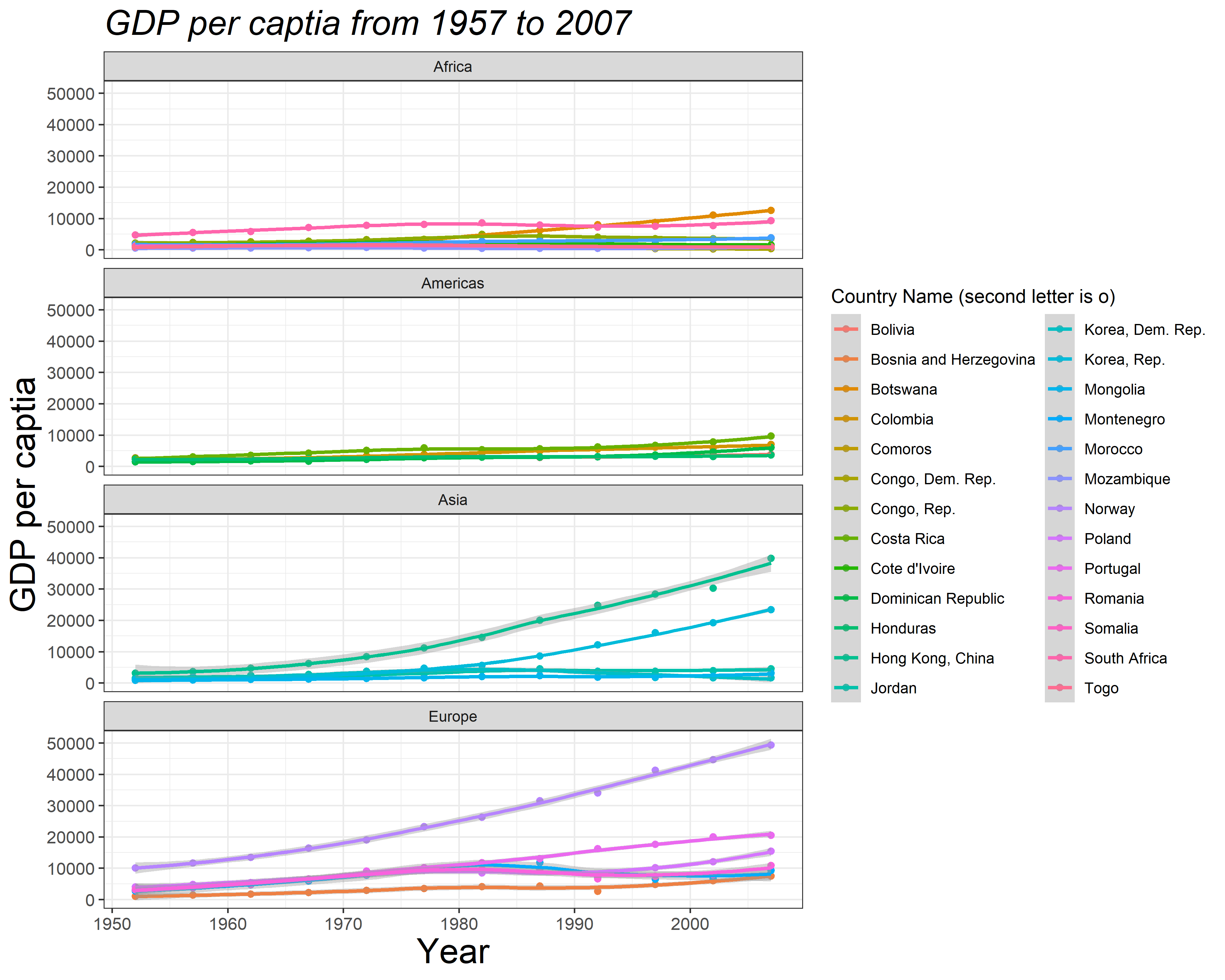

Let’s split our plot into two facets based on

continent:

# Using the facets

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country) ) +

geom_point() +

geom_smooth() +

labs(title="GDP per captia from 1957 to 2007", x="Year", y="GDP per captia") +

theme_bw() +

theme(plot.title=element_text(size=20, face="bold"),

axis.text.x=element_text(size=10),

axis.text.y=element_text(size=10),

axis.title.x=element_text(size=20),

axis.title.y=element_text(size=20)) +

scale_color_discrete(name="Country Name") +

facet_wrap( ~ continent)## `geom_smooth()` using method = 'loess' and formula = 'y ~ x'

One way to change the layout the facets is specifying

ncol and nrow options in the

facet_wrap() function:

# Using the facets - 2 rows (2x1)

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country) ) +

geom_point() +

geom_smooth() +

labs(title="GDP per captia from 1957 to 2007", x="Year", y="GDP per captia") +

theme_bw() +

theme(plot.title=element_text(size=20, face="bold"),

axis.text.x=element_text(size=10),

axis.text.y=element_text(size=10),

axis.title.x=element_text(size=20),

axis.title.y=element_text(size=20)) +

scale_color_discrete(name="Country Name") +

facet_wrap( ~ continent, nrow=2)## `geom_smooth()` using method = 'loess' and formula = 'y ~ x'

7. Saving the plot

Finally, you can save the above plot uisng the ggsave()

function. The default is to save the last plot that you displayed, using

the size of the current graphics device. It’s smart enough to guess the

type of graphics device from the extension. Let’s save the above figure

to a local path D://ese335 with a name

myplot.png:

# Save a ggplot figure

gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country) ) +

geom_point() +

geom_smooth() +

labs(title="GDP per captia from 1957 to 2007", x="Year", y="GDP per captia") +

theme_bw() +

theme(plot.title=element_text(size=20, face="bold"),

axis.text.x=element_text(size=10),

axis.text.y=element_text(size=10),

axis.title.x=element_text(size=20),

axis.title.y=element_text(size=20)) +

scale_color_discrete(name="Country Name") +

facet_wrap( ~ continent, nrow=2)

ggsave("myplot.png") # save a stored ggplotYou can also change the plot size (width and

height) and resolution (dpi) by setting

corresponding options. Use ?ggsave() for more.

# Save a ggplot object

plot1 <- gapminder %>%

dplyr::filter( continent=="Asia" | continent=="Europe" ) %>%

dplyr::filter( substr(country,1,1)=="C" ) %>%

ggplot( aes(x=year, y=gdpPercap, color=country) ) +

geom_point() +

geom_smooth() +

labs(title="GDP per captia from 1957 to 2007", x="Year", y="GDP per captia") +

theme_bw() +

theme(plot.title=element_text(size=20, face="bold"),

axis.text.x=element_text(size=10),

axis.text.y=element_text(size=10),

axis.title.x=element_text(size=20),

axis.title.y=element_text(size=20)) +

scale_color_discrete(name="Country Name") +

facet_wrap( ~ continent, nrow=2)

# And later save it to a stored figure

ggsave("myplot2.png", plot=plot1, width=20,

height=10, units="cm", dpi=400)ggplot2’s grammar of graphics and beyond

We have covered some basics but critical steps of making plots with

ggplot2. There are many more features that we don’t have

time to go through in just one section. You can explore the full

functionality of ggplot2() by studying the further

reading listed at the end.

To summarize, ggplot2’s grammar of graphics goes

like:

# ggplot functions

ggplot(data = <DATA>) +

<GEOM_FUNCTION>(

mapping = aes(<MAPPINGS>),

stat = <STAT>,

position = <POSITION>

) +

<COORDINATE_FUNCTION> +

<FACET_FUNCTION>

# Save a ggplot figure

ggsave() The template takes seven parameters, the bracketed words

that appear in the template. We have no time to cover STAT,

POSITION, and COORDINATE_FUNCTION, which you

can learn by yourself following the further

reading. In practice, you rarely need to supply all seven parameters

to make a plot because ggplot2 will provide useful defaults

for everything except the data, the mappings, and the geom function.

The seven parameters in the template compose the grammar of graphics, a formal system for building plots. The grammar of graphics is based on the insight that you can uniquely describe any plot as a combination of a data set, a geom, a set of mappings, a stat, a position adjustment, a coordinate system, and a faceting scheme.

With this, you can make any type of plot with

ggplot2()!

R Graph Gallery

A good way to learn ggplot2 is to browse plots (and

scripts!) in the R Graph Gallery, such as:

- The R Graph Gallery

- Top

50

ggplot2Visualizations ggplot2extensions- Plotly R Open Source Graphing Library

Find the plots you want to mimic, edit and customize the scripts based on your need.

In-class exercises

Exercise #1

Can you reproduce the following figure (myfirstplot.png,

width 25 cm, height 20 cm, and dpi 400) with ggplot2?